Rice features heavily on our plates. It is the leading cereal crop in terms of meeting human food needs and the third most harvested crop after common wheat and maize. Globally, no less than 523 million tonnes were consumed in 2024, representing three-quarters of available supplies, according to data from the International Grains Council (IGC). Among the countries that consume the most are China and India, which account for a total of 143 and 115 million tonnes per year, respectively.

In terms of production, there has been a steady increase in harvest volumes over the past decade or so, with regular record highs. In 2021, the 500 million tonne mark was reached. Then, in 2024, 524 million tonnes were produced. The ICC forecasts production of 541 million tonnes in 2025 and estimates of around 542 million tonnes in 2026.

However, global warming is not without consequences for harvests. The effects of El Niño have disrupted production in the main producing countries of China, Thailand and Indonesia. The decline in their national production has been offset by an increase in acreage in Africa, North and South America, particularly Brazil.

Rising consumption

Global rice consumption is increasing. Between 2017 and 2024, it rose from 484 to 524 million tonnes. Africa accounts for more than 8% of global rice consumption, which has been growing steadily since 2017, driven by Nigeria (7.7 million tonnes), Egypt (4.1), Guinea (3.2) and Madagascar (3.1). More broadly, Asia and Africa are the two major importing regions in the world, accounting for nearly 80% of global rice flows. The EU accounts for only a marginal share of global consumption, with just 3.2 million tonnes, of which 2.2 million tonnes are imported.

Given that rice is one of the main plant-based food sources for human consumption, international trade is not as high as for wheat. It is mainly consumed within the producing country itself. For example, China, despite being the world’s leading rice producer, exports only a very small amount, averaging 1 to 2 million tonnes. In comparison, the United States, with an average annual production of around 5 million tonnes, exports more rice, with 2 to 3 million tonnes each year.

Thus, in 2024, with 57 million tonnes traded, only 10% of production was exported, compared with 27% for soft wheat.

Rice prices buffeted by global instability

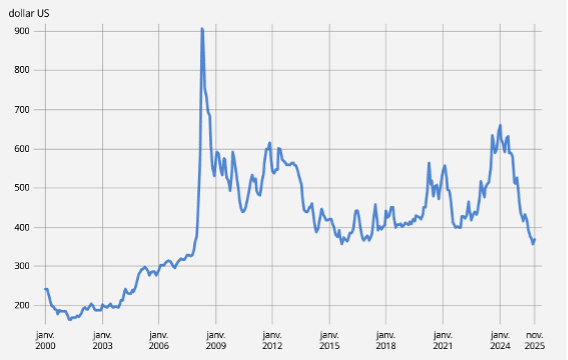

Having reached record highs during the 2007–2013 financial crisis, then suffering the effects of geopolitical instability, the price of this white grain had fallen to £360 in December 2025, a drop of 35% in a single year. (Figure 1). Countries that are heavily dependent on rice for food have been experiencing these fluctuations for the past fifteen years, putting the quantities of rice imported at risk. From now on, agricultural commodity markets must be understood through the lens of extra-economic parameters, such as climate and, even more so, geopolitics.

Source: INSEE and World Bank

India and the global market

Looking at the hierarchy of exporters, India ranks as the global leader, far ahead of Thailand, Vietnam and Pakistan. In 2024, New Delhi shipped 14.4 million tonnes, or a quarter of total global exports, a position that gives it a decisive role in the evolution of this global market.

Deeply committed to ensuring its national food security, New Delhi has used several public policy tools to achieve this, including a strategy of voluntary export restrictions. The combination of climate shocks and the war in Ukraine have led it to restrict its rice exports. From an average of 21 million tonnes between 2021 and 2023, they will fall to 14 million in 2024. In seeking to contain the impact of soaring prices on its domestic market, India has ultimately exacerbated tensions on the global market. However, the ICC’s 2026 projections indicate that Indian rice exports could return to their previous level of 22 to 23 million tonnes.

This political decision, which is certainly aimed at protecting Indian consumers, is inextricably linked to geopolitical turmoil. The war in Ukraine, as well as regular skirmishes on the border with China, are on the political and economic agenda of India, which, although self-sufficient, is not completely immune to food risk.