When we talk about commercial space services, what are we referring to?

Stefaan De Mey. Today, space – or rather LEO (Low Earth Orbit) – is 90% commercial and 10% institutional. The commercial part includes everything that concerns telecommunications, navigation, broadcasting, and their applications. Beyond that there are also institutions who fund infrastructure and satellite constellations. For example, the US Department of Defense has funded the GPS and the European Union funded the Galileo navigation system and Earth observation satellites known as Copernicus. Even though they are government-funded, these infrastructures are used for commercial applications. As such, they represent a large volume of economic activity – an extension of the terrestrial economy in space, with commercial applications on the ground.

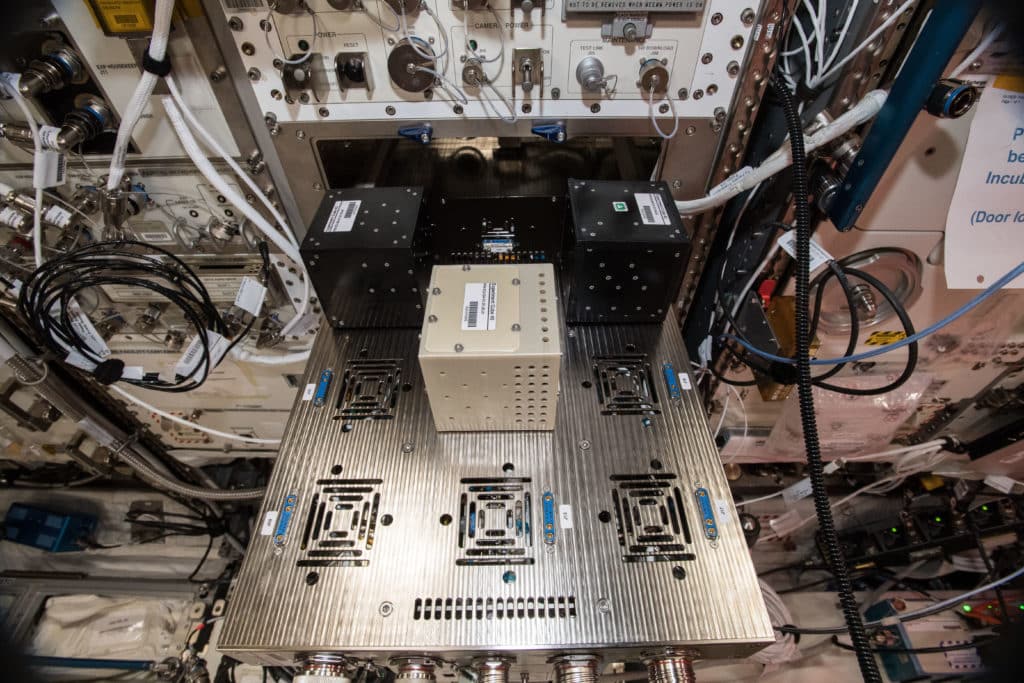

We are now at the stage of integrating the Moon and human spaceflight into that economy – something which is starting to happen with the arrival of space tourism. At ESA, we also want science and research to be part of this economy, considering that space provides an environment for scientific work. Microgravity makes it possible to produce things in space not possible on Earth, such as certain types of crystals, special materials, or artificial organs. The antiviral Remdesivir, for instance, was tested in an “ICE Cube” (International Commercial Experiments), a scientific experiment contained in a 10-centimetre cube sent on board the International Space Station (ISS).

Are large exploration infrastructures still funded by institutions and agencies?

This situation is changing. Over the past 20 years, governments have invested heavily in the ISS. But now the private sector is taking over. In the United States, companies are already building modules that attach to the station and serve as bases for future private stations. On a smaller scale, this is what the European Space Agency is proposing with public-private partnerships in which the private partner provides an all-in-one service, including transport to the space station, installation of the modules (which are standardised) and basic resources such as a broadband link for data transmission, power supply or sample recovery. It is a partnership that opens access to the ISS, optimises its operation and speeds up research.

Europe has basic infrastructure for conducting scientific experiments in space, but it is not fully utilised thus presenting a viable opportunity for a private partner to create a commercial service by offering this infrastructure to customers when it is not being used by the agency. That being said, industry partners can also build new infrastructure to add to that.

Bartolomeo is an example of an ‘integrated’ service that we have developed in partnership with Airbus Defence and Space. The development and operation of which are entirely run and funded by industry, with ESA providing resources available such as transportation, data exchange between Earth and space, and space on the Columbus module. This platform is docked to the European Columbus module and laboratory outside the ISS. It allows companies and research centres to conduct experiments and work in space in the form of payload modules, designed to develop new materials, test technologies, or observe Earth or outer space. In addition, customers but can approach Airbus directly – who provide the end-to-end – service without going through ESA.

What does ESA expect from such commercial services?

We have three objectives. Firstly, we want the scientific community to carry out work on our microgravity platforms to facilitate terrestrial research and to open up this tool to new communities such as industrial R&D. Secondly, as an agency, we need to continue learning how to prepare our platforms for future exploration missions to the Moon and then to Mars. It is important to mention that, in a commercial context, the agency becomes one of many customers, with other users (scientists and industry) procuring the services they need directly. Finally, we want to avoid a situation where only American companies are present in low Earth orbit and our companies and researchers must go through them. This is a new market where we want to be present by building on our experience of the ISS.

Today, the customer buys a turnkey, end-to-end service. NASA, for example, buys from SpaceX the transport of n tonnes or four astronauts to the station. The US currently dominates the transportation market with reusable launchers. Europe needs to think about the next phases and prepare for the ‘post-Ariane’ era. We developed the Automated Transfer Vehicle launched by Ariane 5, which has resupplied the ISS five times and was one of our contributions to the partnership, allowing us access to the station. To reposition ourselves in today’s space market, we need to innovate and develop new services.

What services does ESA offer (or plan to offer)?

We currently offer three commercial services in low Earth orbit and are preparing others for what we call the ‘future lunar economy’. In addition to Bartolomeo, Space Applications Services SA markets ICE Cubes. These cubes, with a standard size of 10 cm on each side, contain various scientific, technological, or even artistic experiments. Researchers have an Internet connection to monitor and control them in real-time. ESA is responsible for transporting the cubes, installing them, and returning them to Earth after four months. The Bioreactor Express is also a turnkey service for experiments conducted for one year in the Kayser Italia Kubik laboratory container. For the ‘post-ISS’ era, we are exploring the possibilities for industry to build and market a complete platform in LEO offering science and habitation functions as a service. In addition, ESA is developing several projects in the framework of the Moon exploration programmes, for example with the German satellite manufacturer OHB, which provides a transport service to the lunar surface. On the telecommunications side, we are currently expanding the capacity of the Goonhilly ground station in the UK to provide commercial deep space communications services on the Moon and beyond. To complement this ground station, we are preparing a constellation of four satellites in lunar orbit. These Commercial Lunar Mission Support Services (CLMSS) will be used for future exploration missions to navigate around the Moon.

Booming space markets

Since the Perseverance rover landed on the surface of Mars in February 2021, Morgan Stanley published a study on the space sector and the promises of the so-called “new space”. According to the Bank of America, the economic weight of the sector should increase from $350bn in 2016 to $1tn dollars in 2040 – a 185% increase! This growth is largely due to the emergence of satellite constellations dedicated to internet access, which were almost non-existent in 2016 and which will represent almost 40% of the sector in 2040. The other developing markets are deep space exploration missions, to the Moon and then to Mars; Earth observation and the study of climate change; the monitoring and ‘cleaning’ of debris, the growing number of which poses a threat to all space objects, mainly in low orbit; and space tourism, which is taking its first steps. Exploration missions are still mainly financed by governments and space agencies. Other markets, however, derive their revenues from the sale of commercial services to government agencies (military and scientific), businesses and individuals: the sale of bandwidth, telecoms, television and soon travel.