When the military capabilities of individual European Union nations are combined, they surpass those of the Russian Armed Forces, particularly in the air and maritime domains. However, Louise Souverbie, a researcher at the IRIS (Institut de relations internationales et stratégiques), stresses that the Kremlin’s strategic assets should not be underestimated: “Integrated air and missile defence (IAMD) systems, as well as their deep strike capability, are real strengths,” before pointing out that these Russian strikes have inflicted significant damage in Ukraine since the start of the war. Indeed, the Russian military has demonstrated its ability to strike military or economic targets located well beyond the front line. Even without being deployed, these long-range strike capabilities can feed into a strategy of intimidation.

Russia’s ballistic arsenal is based on a range of missiles. With a range of around 500 km, the Iskander ballistic missiles are the most widely used. The Kinzhal missile (range of 2,000 km) has been presented by Russia as invincible, although it has been intercepted on several occasions by the Ukrainian army. As for the Oreshnik missile that struck Dnipro last year, it is reported to have a range of 3,000 to 5,000 km. The Russian defence arsenal also includes intercontinental missiles, primarily reserved for nuclear warheads.

Combating inexpensive yet destructive drones

The Russian Armed Forces have turned drones into a key asset. The Iranian-made Shahed model, which is inexpensive (costing just a few tens of thousands of euros) and capable of striking targets up to 2,500 km away, has become central to their strategy. According to Louise Souverbie, “the Shahed drone has shifted the balance of power by creating a cost asymmetry between offensive and defensive capabilities.” This disparity is also evident in the Red Sea, in the conflict with the Houthis.

To counter drone salvos, whose effectiveness relies on a saturation-exploitation strategy (saturating defences with a salvo of low-cost drones or missiles, followed by exploitation and strikes using a few more precise missiles), the EU must develop diversified interception capabilities to avoid relying solely on particularly costly interceptors. “For example, the interceptors used in the Franco-Italian SAMP/T system, or the American Patriot system, each cost between €2 and 5 million.”

More broadly speaking, European states have acquired equipment based on cutting-edge technologies, whilst Russia has prioritised quantity. In light of this, European defence forces are seeking to develop “multi-layered” air defence capabilities, combining very short‑, short‑, medium- and long-range interception systems and incorporating less expensive solutions alongside state-of-the-art systems.

Production capacity: what changes are afoot?

Whilst information coming out of Moscow should be treated with caution, several reports1 highlight the rapid and significant growth in Russia’s defence production capacity. By shifting to a war economy model, “the Kremlin has managed to create a centralised system, involving requisitions, restrictions on workers’ rights and the mobilisation of the entire Russian industry to support the war effort, whilst investing heavily in the creation of new production lines and even new production sites. For example, Russia now manufactures Shahed drones (known as Geran in Russia) itself at least two new sites in Tatarstan,” explains Louise Souverbie.

Despite the international sanctions in force, Russian industry has managed to secure its supplies of strategic electronic components. “A network of companies has been established, such as in Kazakhstan, to import technologies and thus circumvent the embargoes with little difficulty”.

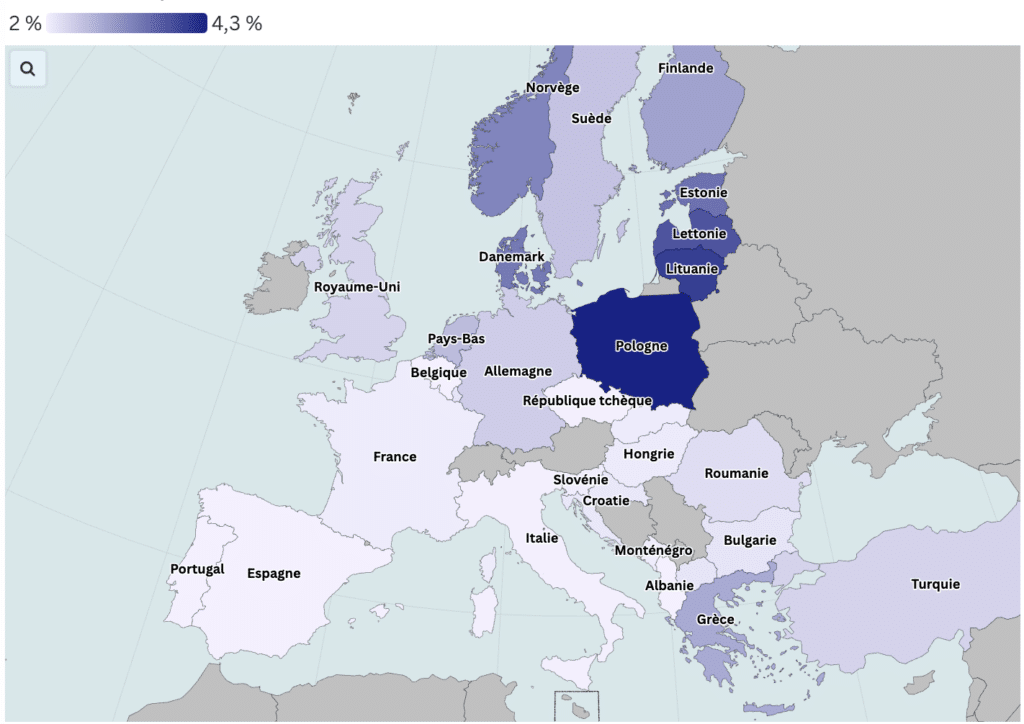

In budgetary terms, 6% of Russian GDP was allocated to defence in 2025. By comparison, on the European side, Poland remains top of the rankings for military spending (4.48% of national GDP), followed by the Baltic states (Lithuania 4%, Latvia 3.73%, Estonia 3.38%), whilst France barely exceeds the 2% of GDP mark. The combined military expenditure of the 32 NATO countries rose to a total of $1,588 billion in 2025.

With the SAFE (Security Action for Europe) Plan, Brussels aims to act on two fronts simultaneously: pooling demand through joint procurement of military equipment, and pooling supply via industrial projects involving companies across several European countries, for example in the field of ammunition3. “A range of tools has emerged since the outbreak of the war in Ukraine in 2022 – ASAP (Act in Support of Ammunition Production) for ammunition production, EDIRPA (European Defence Industry. Reinforcement through common. Procurement Act) for joint procurement – but until now these schemes have relied on grants and remained on a modest scale,” adds the IRIS researcher. The SAFE Plan, adopted as a regulation in May 2025, proposes a new mechanism and a new scale.

Long-term loans (up to 45 years) replace grants. With a budget of €150 billion in loans, this mechanism is part of the ReArm Europe plan (March 2025, since renamed Readiness 2030), which envisaged releasing €800 billion for European defence. The Commission has already approved the national funding plans of 16 countries, including Estonia, Poland, Italy and Finland. This mechanism is based on eligibility criteria designed to support European industry whilst maintaining a degree of flexibility for certain critical capabilities.

Towards strategic autonomy?

According to estimates by SIPRI (Stockholm International Peace Research Institute), between 2020 and 2024, half of all military equipment is imported from outside the EU. Of these purchases, 64% are believed to come from the United States. To address this strategic weakness, the eligibility criteria for accessing loans under SAFE are targeted: at least 65% of the value of the components of any equipment purchased must be of European, Norwegian or Ukrainian origin.

Eligible projects are divided into two categories: “consumables and standard equipment”4 (ammunition, missiles, artillery), and complex weapon systems (air defence and anti-missile systems, strategic catalysts, AI, quantum technology). For this second category, European companies awarded the contract must be able to develop the product without the involvement of a third country. “This clause aims to strengthen a form of strategic autonomy by ensuring companies’ ability to adapt and modernise European equipment entirely independently,” concludes Louise Souverbie.

Alicia Piveteau

Such as those produced by the Royal United Services Institute for Defence and Security Studies, or the Foundation for Strategic Research

https://www.rusi.org/explore-our-research/publications/occasional-papers/winning-industrial-war-comparing-russia-europe-and-ukraine-2022–24↑