Chips Act: can Europe catch up in the global semiconductor race?

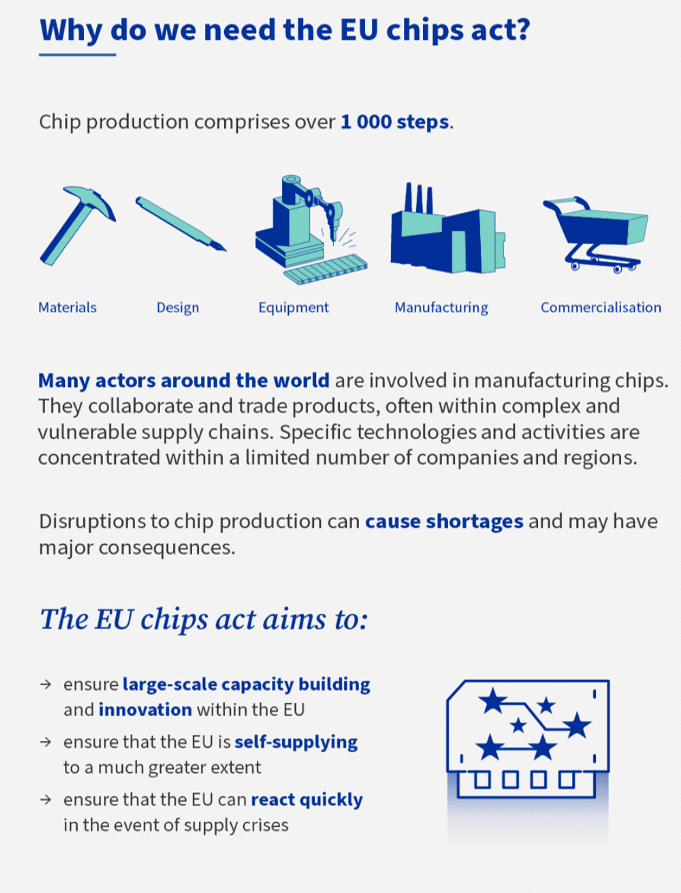

- Adopted by the EU in 2023, the Chips Act aims to strengthen the continent’s industrial capabilities and reduce certain strategic dependencies.

- It aims to mobilise up to €43 billion in investment and increase the European Union’s share of global semiconductor production to 20% by 2030.

- Around fifteen years ago, European manufacturers gradually stopped competing in the technology race, leaving the field open to American and Asian players.

- Europe therefore does not currently have the human resources needed to rapidly deploy several state-of-the-art mega-factories.

- On the other hand, it has large, solid industrial groups, but it still lacks a dense network of start-ups capable of producing the sector’s future leaders.

Since shortages caused by the Covid-19 health crisis, the high concentration of production in Taiwan and the Sino-American technology war over artificial intelligence, semiconductors have occupied a special place in industrial policy. Found in smartphones, data centres, vehicles, medical equipment and defence systems, they account for a growing share of technological investment and sovereignty strategies1.

In this landscape dominated by a handful of players capable of producing the most advanced chips, Europe finds itself in a very specific position. The continent has leading companies in certain segments of the value chain, starting with ASML in EUV lithography, but remains absent from the manufacture of the most advanced nodes, a sector currently dominated by TSMC and Samsung2. This situation has led the European Union to adopt the Chips Act, which aims to strengthen the continent’s industrial capabilities and reduce certain strategic dependencies3. However, the challenge is not limited to building new factories or mastering the most miniaturised manufacturing processes.

Some of the work currently being carried out in industry and research focuses on other technological pathways, notably around chiplets, heterogeneous integration and advanced component assembly techniques4. These approaches make it possible to combine, within a single system, technological building blocks developed using different processes, rather than simply continuing the race towards miniaturisation.

The European Chips Act at a glance

Adopted in 2023, the Chips Act is the European Union’s flagship initiative in the semiconductor sector. It aims to mobilise up to €43 billion in public and private investment and to increase the European Union’s share of global production to 20% by 2030. The scheme supports research, industrial capacity and the security of supply chains. Several major projects have already been announced, notably in Germany, France and Italy.

As Scientific Director of the “Integration and Packaging” programme at CEA-Leti, Pascal Vivet has been working on advanced semiconductor integration technologies for numerous years5. His research focuses in particular on three-dimensional architectures, chiplets and assembly processes that enable different electronic functions to be combined within a single system. Notable among these projects is the IntAct project, which is dedicated to new multi-core architectures based on the three-dimensional stacking of chiplets6.

Why are people already talking about a Chips Act 2.0?

Whilst the first projects supported by the Chips Act are still being rolled out, several European officials and industry players are already discussing a second phase of the European semiconductor strategy.

The first phase focused largely on production capacity and industrial investment. Current discussions are centred more on funding for design companies, skills, research, advanced integration technologies and sectors where Europe already holds a strong position.

No official initiative has yet been adopted under the name “Chips Act 2.0”. The term is, however, increasingly being used to refer to this possible evolution of European semiconductor policy.

Today, Europe does not produce the most technologically advanced chips, whilst some global players are already manufacturing them at 3 nm. In your view, what are the technological obstacles behind this gap?

Historically, Europe possessed expertise in the most advanced technologies, driven in particular by STMicroelectronics, Infineon and NXP. But around fifteen years ago, European manufacturers gradually stopped pursuing this technological race, leaving the field open to American players (such as Intel) and Asian players such as TSMC and Samsung, who were the only ones capable of mobilising the massive investments now required.

The current gap is more a matter of investment than a technological shortfall. Europe retains world-class expertise, particularly in lithography through ASML. At CEA-Leti, work is continuing on advanced FD-SOI pilot lines around the 10 nm mark, with the aim of transferring these innovations to industry. Achieving more advanced technology nodes therefore remains possible. Moving from 28 nm or 18 nm, currently used industrially in Europe, to 10 nm or 7 nm would already represent a considerable technological leap. The real question is what resources Europe is prepared to commit to this ambition.

The value chain relies on a few highly concentrated links, such as ASML for EUV lithography, TSMC for advanced manufacturing, and Cadence, Synopsys and SIEMENS for design. In your view, what is the most critical bottleneck for Europe if it is to genuinely achieve greater autonomy?

The main vulnerability lies in the ecosystem of design companies, the fabless companies [editor’s note: companies without their own factories], which develop new circuit architectures and new systems. It is often within these organisations that the most disruptive innovations emerge. Europe has large, robust industrial groups, but it still lacks a dense network of start-ups capable of nurturing the sector’s future leaders. The United States has long benefited from a particularly dynamic ecosystem, supported by venture capital capable of rapidly fuelling the growth of innovative companies. Two examples worth noting are start-ups designing AI accelerators using advanced technologies, such as AXELERA (in the Netherlands) and VSORA (in France).

The Chips Act aims to address these challenges by creating shared design platforms, providing common tools and open technology libraries7. However, the main difficulty remains the ability to finance the scaling up of these companies. European start-ups often have the necessary skills and ideas, but struggle to scale up quickly enough to compete with their American or Asian rivals. The problem is therefore not so much technological as financial. Europe is still struggling to rapidly transform its innovations into leading industrial players.

Fabless companies, foundries, equipment manufacturers: who does what in the semiconductor industry?

Chip manufacturing relies on several distinct sectors. So-called fabless companies design electronic architectures but do not own manufacturing plants. NVIDIA, Qualcomm and AMD operate according to this model. Foundries, such as TSMC and Samsung, physically produce the chips for their customers.

Other players supply electronic design tools, such as Cadence, Synopsys and SIEMENS, a European CAD company, or the industrial equipment required for manufacturing, such as ASML for lithography. This increasing specialisation explains why no single company currently controls the entire global value chain.

Europe has a proven advantage in FD-SOI thanks to STMicroelectronics and GlobalFoundries. Can this position serve as a genuine pillar of technological sovereignty, or are we confined to a segment that is too limited to compete with advanced CMOS?

FD-SOI is a real asset for Europe, even if it does not cover all its needs. For high-performance computing applications, data centres or the most advanced artificial intelligence infrastructure, cutting-edge CMOS remains indispensable. On the other hand, for fields such as quantum computing, microcontrollers, imaging, sensors, low-power applications or cybersecurity, FD-SOI offers significant advantages and can be a key differentiating factor. Provided the necessary investment continues, this technology can therefore represent a strategic pillar across a range of major industrial applications.

Building an advanced semiconductor factory takes years and requires highly specialised skills. Does Europe currently have the human and industrial resources needed to scale up capacity, or is there a risk of underutilisation?

The issue of skills is one of the main challenges. At present, Europe does not yet have the human resources required to rapidly roll out several state-of-the-art mega-factories. This is precisely one of the issues addressed under the Chips Act. In France in particular, significant efforts are underway in universities, engineering schools, research organisations and laboratories to increase training capacity and the number of graduates in fields related to microelectronics. But developing the skills required for an industry of this scale takes time. Even with adequate industrial investment, building up human resources is a long-term process.

The European Chips Act aims for 20% of global production by 2030. From a strictly technological perspective, setting aside political considerations, do you think this target is achievable?

It is difficult to assess, as industrial trajectories depend so heavily on technological, human and political factors. Beyond the technological challenges themselves, we must consider the time required to ramp up production, recruitment difficulties and the complexity of European decision-making processes. The political will is there but translating it into operational action is often a slower process. The target is ambitious and sends an important signal to European industry. As for whether it will be achieved by 2030, it is still too early to say.

Within the global value chain, certain components remain virtually impossible to replace, such as ASML’s EUV equipment or certain high-purity materials produced by only a handful of suppliers. Of these dependencies, which do you believe is currently the most critical for Europe if it is to secure its production capacity in the long term?

No single technological bottleneck currently appears to be preventing Europe from moving forward. Access to ASML’s EUV equipment, for example, remains assured as it is a European technology. The main obstacles seem to lie more in the areas of investment, skills, industrial organisation, design capabilities and the development of the entrepreneurial ecosystem.

In the current geopolitical context, characterised by mounting international tensions and a resurgence of concerns over sovereignty, Europe nevertheless has a significant opportunity. Growing demand in the defence, space and critical infrastructure sectors is creating a favourable environment for the development of new industrial capabilities. Even if Europe lags somewhat behind in the most advanced processes, the investments made today could yield significant results within the next 5 to 10 years.

Why is advanced manufacturing concentrated in Taiwan?

The most advanced chips require considerable industrial investment. A single factory can cost tens of billions of euros. Over time, only a few players have retained the financial and technological capabilities needed to keep up with this race, notably TSMC and Samsung. This concentration explains why semiconductor production has become a matter of national sovereignty for many countries.

The race for semiconductors is often seen as a race to master the most advanced technology nodes. Does this view truly reflect the industrial challenges facing the sector today?

Not entirely. The focus on the most advanced technology nodes sometimes provides an incomplete picture of current industrial challenges. One of the major developments in the sector concerns heterogeneous integration, that is, the ability to combine several specialised technologies within a single system. The aim is no longer simply to manufacture a single, ever-more-miniaturised chip, but to assemble different chiplets specifically dedicated to computing, memory, sensors, power management, cybersecurity or communications.

3D integration and advanced packaging technologies make it possible to bring these different technological building blocks together. In this field, Europe already has significant strengths. CEA-Leti in France, as well as several organisations in Germany and Belgium, have been developing recognised expertise in these fields for several years. This approach can meet the needs of strategic European sectors such as the automotive, aerospace and defence industries, quantum computing, AI, communications and sensors, whilst limiting the costs and risks associated with the constant race for the most advanced processes.

Chiplets: a different approach to semiconductor design

Rather than integrating all functions onto a single chip, the chiplet approach involves assembling several specialised components, such as computing, memory, sensors or security, using their respective technologies. Combined with 3D integration and advanced packaging technologies, chiplets offer greater flexibility and enable different manufacturing processes to be combined within a single system. This approach is now playing an increasingly important role in the semiconductor industry.

Does Europe have any particular strengths it could draw on to strengthen its position in the global semiconductor ecosystem?

Europe has strong positions in several areas that complement the semiconductor sector itself. Embedded software, embedded systems, cybersecurity and technologies for protecting digital infrastructure are sectors in which European players possess recognised expertise. These capabilities are essential for securing data centres, cloud infrastructure, public services and critical industrial systems. They represent important levers for technological sovereignty and enable Europe to maintain strong positions in high value-added segments.

In practical terms, if Europe were to decide to significantly increase its investment in semiconductors and related technologies, which areas should be prioritised?

This question is currently the subject of much debate within the European ecosystem. Quantum computing is already attracting significant investment. Industrial applications are still some way off, but failing to invest today would mean falling behind in a way that could prove irreversible tomorrow.

In the semiconductor sector, another key question concerns advanced CMOS. Should Europe develop its own capabilities, or should it attract more advanced production to European soil to secure strategic supplies?

Both approaches remain on the table. At the same time, Europe would benefit from stepping up its investment in areas where it already has competitive advantages: heterogeneous integration, FD-SOI, the Internet of Things, industrial robotics, Industry 4.0, cybersecurity and technologies for the healthcare sector. Microelectronics now lies at the heart of all these ecosystems. Strengthening these sectors therefore amounts to strengthening European technological sovereignty more broadly.